AI will tell you that the best 401(k) money can buy has low fees but I take exception to this. A plan sponsor is expected to act in the best interest of participants, and the best interest of participants is for the plan sponsor to pay for most if not all fees associated with plan administration. Plan sponsors who pay most if not all fees are going to look for the best service their money can buy.

AI will tell you that the best 401(k) money can buy has low fees but I take exception to this. A plan sponsor is expected to act in the best interest of participants, and the best interest of participants is for the plan sponsor to pay for most if not all fees associated with plan administration. Plan sponsors who pay most if not all fees are going to look for the best service their money can buy.

The best plan that money can buy necessarily delivers superior outcomes for participants, in terms of their ability to retire comfortably and at a reasonable age.

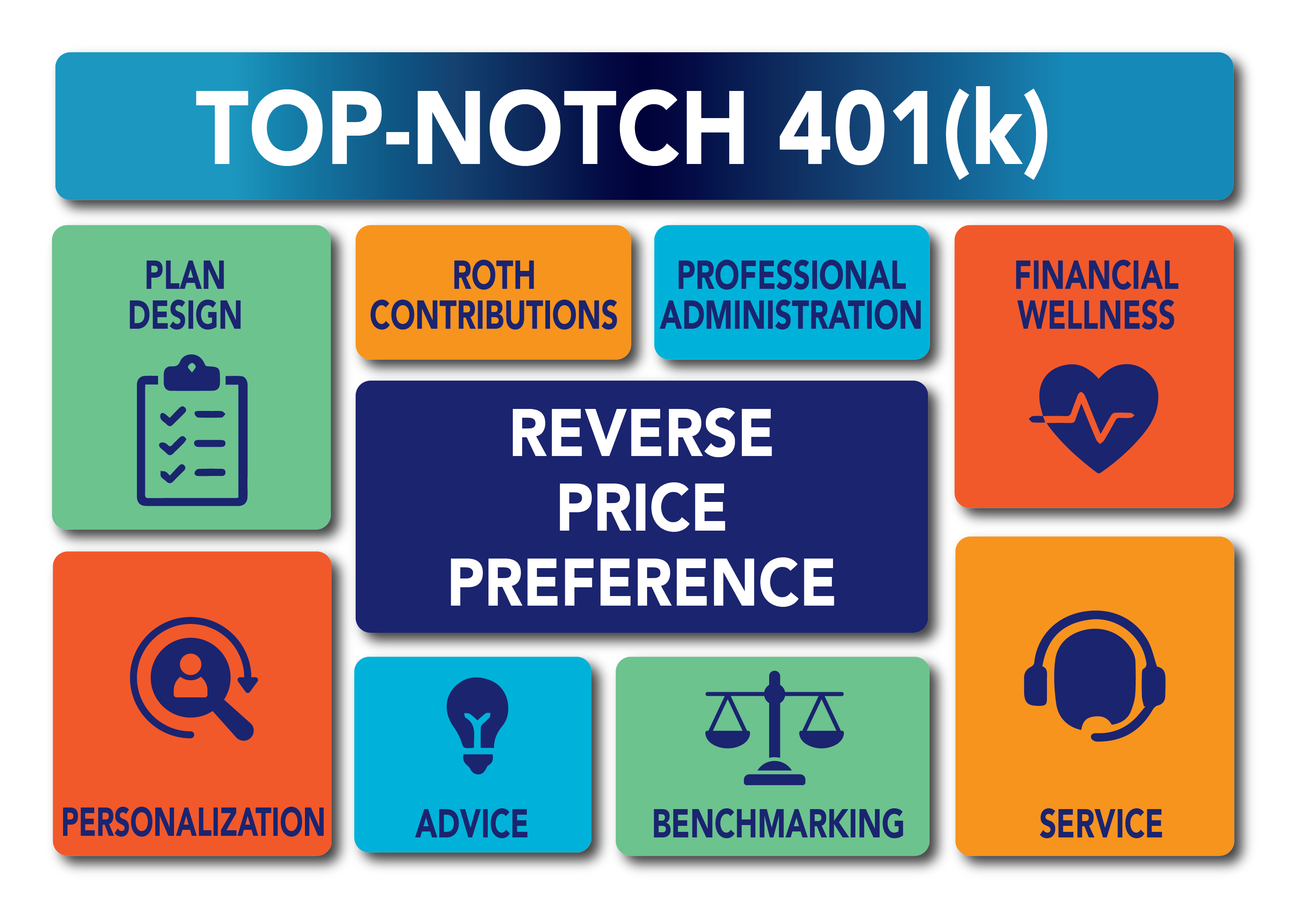

- Plan design – money purchase or cash balance plan, combined with a 401(k) plan, and an NQDC plan for highly compensated employees and those earning more than $145,000 who are constrained by legislation. Default options that will lead participants to success (especially long-time employees who entered the plan late, or did not save enough for retirement for no fault of their own).

- Roth contribution types are a necessity post SECURE 2.0, to allow employees with FICA wages over $145,000 to make catch up contributions. Roth account balance accumulate tax deferred, and are not subject to income tax at the time of distribution. Roth is a tax-efficient alternative to retail brokerage accounts invested in equity with a buy-and-hold strategy to avoid short-term capital gain tax liability.

- Comprehensive financial wellness counseling to guide participants in a wide range of life situations through tough financial decisions caused by personal hardship, dependent care responsibilities, unfavorable tax treatment, or exceptional exposure to cyberfraud

- Personalizable investment options, including asset allocation models that include an allocation to alternative asset classes uncorrelated with bond or equity returns. Yes, that might include an allocation to private equity, private real estate, private debt, and maybe perhaps select crypto investments.

- Retirement income counseling that encompasses all options available – in and out-of plan – to act in the best interest of participants, and to empower pre-retirees to access retirement success regardless of stage in the equity market cycle.

- Professional administration. If the plan sponsor does not employ a dedicated retirement plan specialist with extensive experience running retirement plans, retain the services of a professional administrator who accepts ERISA 3(16) fiduciary, and maybe even 402(a) fiduciary status. Why not? These services can be obtained through a Pooled Plan Provider in the context of a PEP plan or in a single employer plan.

- Exceptional plan sponsor service – Client Relationship Manager who reports to the plan fiduciary and delivers recommendations to decision makers that help them act in the best interest of participants and responsive day-to-day account manager who answers questions promptly. Both act as a well connected team that communicates frequently, leveraging technology such as Salesforce and MS Teams.

- Plan and investment advice from the very best. The best plan advisors are connected with the best stakeholders in the industry and know how to create partnerships that enhance total value, not just the sum of its parts. Specialists have the knowledge to discern superior quality from low-cost, and at-par service performance.

- Frequent benchmarking to verify that outcomes are in the top decile, and services are top-notch, up-to-date, and the best that money can buy.

Yes, the solution could be the most expensive in the market. When the plan sponsor covers all the fees, considering only cost does not act in the participants' best interest. For sponsors so fortunate to operate in a sector or market that requires the best talent that money can buy, indeed, the retirement plan also should be the best that money can buy, and it could be the most expensive option available. Why wouldn’t you get the best for your employees if you can afford it?

If your employees merit it and you can afford it, buying them a Rolex® time piece at retirement is a great choice.